Fdic Vs Sipc Insurance

/personal-capital-vs-vanguard-personal-advisor-services-4dad1d34084c4780aec788ace455b4a3.jpg)

Personal Capital Vs Vanguard Personal Advisor Services Which Is Best For You

How Does M1 Finance Make Any Money Investing Simple

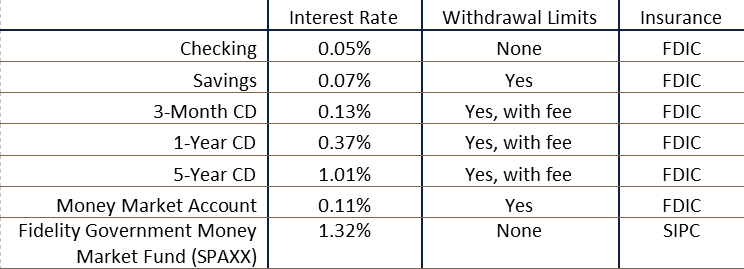

Fixed Income

Fdic Or Sipc How Should I Insure My American Company S Money Gpl Tax Accounting

Federally Insured Deposits Archives Ironwood Wealth Management

Fdic Vs Sipc Understanding Your Account Insurance Marcus By Goldman Sachs

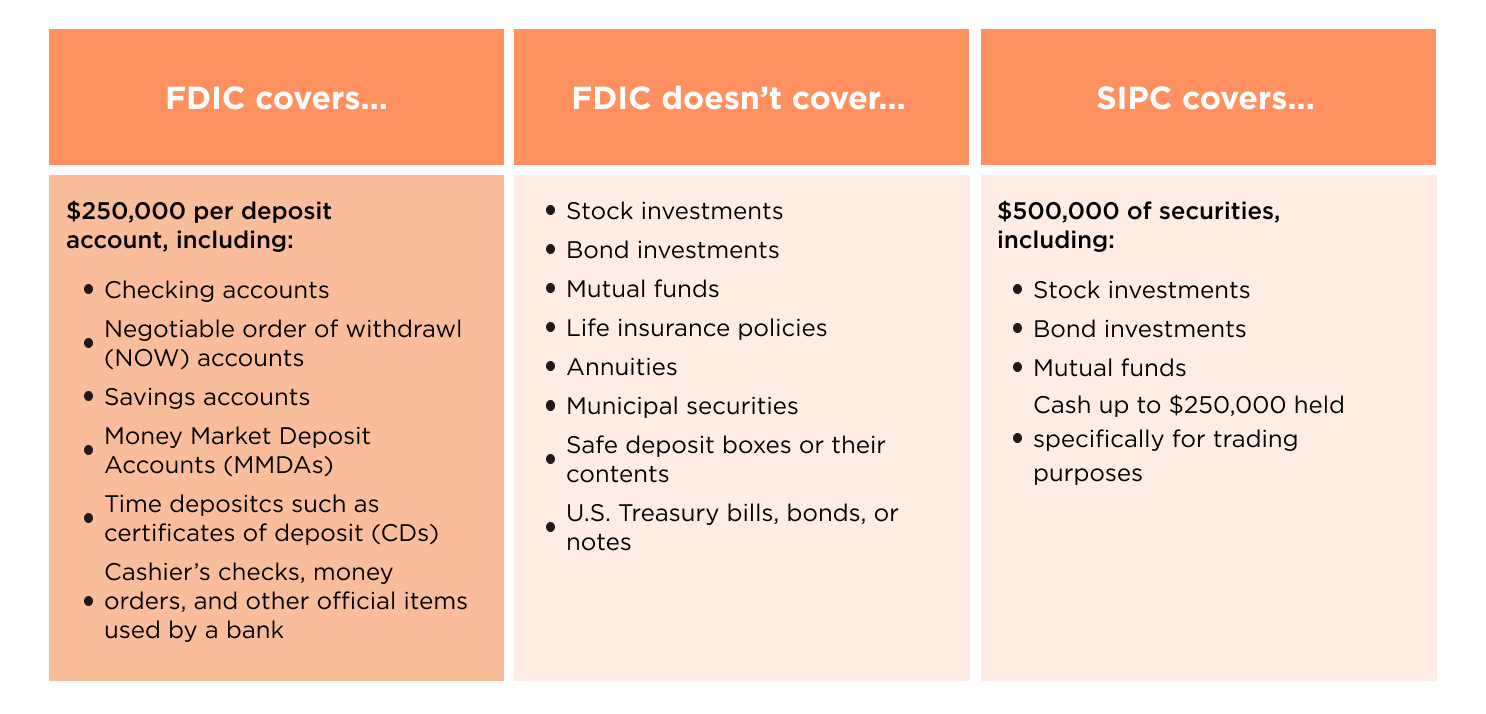

Securities investor protection corporation just like how the fdic insures bank deposits in the event of a bank failure sipc insures investment accounts in the event of a failure.

Fdic vs sipc insurance. The federal deposit insurance corporation ah there it is was founded in 1933 as an independent agency of the us. Alexa what is fdic. Federal deposit insurance corporation fdic insurance and securities investor protection corporation sipc offer two different types of coverage that help protect your assets. Fdic and sipc are both a type of insurance that offers protection for your money but thats where the similarities end and the explaining begins.

Fdic and sipc insurance coverage. In the case with sipc accounts are insured up to 500000 per account. Take a moment to think about all the different types of insurance you currently have. Sipc on the other hand aims to protect up to a certain amount of losses if your brokerage firm fails.

These types of insurance operate very differently. This includes 250000 in cash. As with the fdic the sipc insures your brokerage account for up to 250000 per account owner. It protects the cash being held in bank accounts up to 250000 per depositor per fdic insured bank.

Fdic insurance does not cover investments in stocks bonds mutual funds life insurance policies annuities municipal securities or money market funds regardless of whether the bank that holds the investments is fdic insured. You may have insurance for your car renters insurance for your apartment and life insurance for well yourself. Sipc insurance covers assets and cash in a brokerage account up to a certain amount. The federal deposit insurance corporation fdic was created in 1933 with a number of goals the most notable being insurance for your bank deposits.

Sipc insurance on the other hand protects your assets in a brokerage account. The fdic and ncua insure cash thats held in banking products up to a certain amount. What each one protects. If your bank has fdic insurance the standard insurance amount is 250000 per depositor per insured bank for each account ownership category.

Here are a few key differences between the two entities. Fdic insurance is the standard deposit insurance offered at most traditional banks for things like checking and savings accounts. Sipc members pay annual premiums into an insurance fund and money held in this fund covers some of your losses if your broker goes bankrupt. Fdic insurance and sipc coverage protect bank and brokerage firm customers respectively against the risk of failing financial institutions.

Adapting The Concept Of Sunscreen To Understand Fdic And Sipc Insurance Iris

Betterment Faces Questions From Regulator After Launching Checking And Savings Account

Understanding Fdic Insurance Vs Sipc Protection Brex Blog

Betterment Vs Fidelity Go Which Is Right For You

Robinhood Lacked Proper Insurance So Will Change Checking Savings Feature Techcrunch

Robinhood Debate Highlights Differences In Fdic And Sipc Protections

Ov4uum35n Dvxm

Here S The Difference Between Fdic And Sipc Insurance And Why You Need To Know Wealthfront Blog

What Is Sipc Insurance Investment Insurance Questions Youtube

Are Money Market Accounts Fdic Insured Ally

Acorns Review 2020 A Safe Worthwhile Investing App

Sipc Insurance What It Does And Does Not Protect Nerdwallet

Fdic Vs Ncua Vs Sipc How Are My Money And Assets Protected

Fdic Vs Sipc Insurance 8 Things You Need To Know Today Chief Mom Officer

Sipc Insurance What It Does And Does Not Protect Nerdwallet

False Comfort Of Sipc Insurance

Robinhood S Cash Management Shows Financial Regulation Is Working Quartz

Sipc Chief Raises Concerns To Sec About Robinhood S Free Checking Accounts

Robinhood Debate Highlights Differences In Fdic And Sipc Protections

Fdic Vs Sipc Coverage And Limits Ally

What Happens If Webull Goes Out Of Business Investing Simple

The Epic Rise And Fast Fall Of Robinhood 3 Checking And Savings Chief Mom Officer

Robinhood All News And Posts By Crowdfund Insider Page 2 Of 3

Fdic And Sipc Insurance Withum

Brex Cash Claims Sipc Protection Checking Poses A Challenge Quartz

Sipc Vs Fdic What S The Difference Magnifymoney

Why Is Fdic And Sipc Insured Important

Robinhood Checking And Savings What We Know

Sipc Vs Fdic What S The Difference Magnifymoney

Sipc Securities Investor Protection Corporation Sipc Insurance

How To Maximize Fdic Coverage Ally

Sipc Insurance What Assets Are Protected

What Is Fdic Insurance History Coverage Limits Rules For Banks

Insurance And Protection Differences Fdic Vs Sipc Betterment

Here S The Difference Between Fdic And Sipc Insurance And Why You Need To Know Wealthfront Blog

Is Merrill Edge Safe Legit Insured Is It Scam Bbb Rating 2020

Can You Insure Your Bitcoin Finivi

How Raymond James Protects Your Accounts

Robinhood Checking And Savings What We Know

Sipc Vs Fdic Understanding The Difference Depositaccounts

Insurance And Protection Differences Fdic Vs Sipc Betterment

Fdic Vs Sipc Insurance 8 Things You Need To Know Today Chief Mom Officer

Robinhood S Yield Busting Savings Accounts May Not Be Insured Bankrate Com

What Is The Securities Investor Protection Corporation Sipc

Back To The Future Stealth Bank Robinhood Offers Fdic Insured Cash Accounts After Previous Balk

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcs2zqun77i0czfeazew05bdtez2yqxzswoy Xxq6grki9t7g Im Usqp Cau

Sipc Insurance Limits An Overview Of How They Work

Sipc Insurance How Betterment Protects Your Investments Betterment

Http Fa Opco Com Hnhpcg Mediahandler Media 191388 Sipcandfdicinsuranceatopco Pdf

What Is Fdic Insurance History Coverage Limits Rules For Banks

/wealthfront-vs-charles-schwab-intelligent-portfolios-dc8b708347dc461fb7dd0970a48de0c3.jpg)

Wealthfront Vs Charles Schwab Intelligent Portfolios Which Is Best For You

What Is Fdic Insurance History Coverage Limits Rules For Banks

What Is The Sipc And What Does It Do Smartasset

Fdic Vs Sipc Insurance What S The Difference Finance Globe

Https Www Lfg Com Wcs Static Pdf Nfs 20bank 20deposit 20sweep 20program 20 Bdsp 20disclosure 20document 20 Pdf

What Is The Fdic Acorns

Fdic Insured Deposit Account Not Covered By Sipc

What The Fdic And Sipc Do And Do Not Protect Haven Life

Insurance For Your Investments What The Sipc Can Do For You

Fdic Vs Sipc Insurance 8 Things You Need To Know Today Chief Mom Officer

Is Fidelity Safe Legit Or Scam Sipc Fdic Insured Bbb Rating 2020

Is Robinhood S Checking Savings Account Safe Is It Worth Switching To It 3 Interest Rate Dargadgetz

Sipc Securities Investor Protection Corporation Sipc Insurance

Why Fintech Cash Accounts Are Drawing Regulators Like Fdic Financial Planning

Franklin Gold Linkedin

Is Your Money Safe Can The Fdic Sipc Protect You

Fdic And Ncua Protect Your Deposits Becu

What Is Fdic Insurance How Can It Protect My Accounts

Here S The Difference Between Fdic And Sipc Insurance And Why You Need To Know Wealthfront Blog

Fdic Vs Sipc Coverage And Limits Ally

What The Fdic Sipc And Finra Mean For Your Investments

Fdic Vs Sipc Insurance 8 Things You Need To Know Today Chief Mom Officer

Insurance And Protection Differences Fdic Vs Sipc Betterment

/wealthfront-vs-td-ameritrade-essential-portfolios-072e85eb93f449cab08317a9625d8776.jpg)

Wealthfront Vs Td Ameritrade Essential Portfolios Which Is Best For You

What Is Sipc Insurance Coverage For Your Brokerage Account

What The Fdic Sipc And Finra Mean For Your Investments

Are Robinhood Accounts Fdic Insured Updated 2020 Investotrend

Is Sipc Insurance Or Fraud Youtube

Understanding Fdic Insurance Vs Sipc Protection Brex Blog

Fdic Vs Sipc Understanding Your Account Insurance Marcus By Goldman Sachs

Headwater Investment Consulting Blog

Fdic Insured Deposit Account Not Covered By Sipc

Sipc What Sipc Protects

Here S The Difference Between Fdic And Sipc Insurance And Why You Need To Know Wealthfront Blog

Investing Money Is Your Money Stocks Bonds And Etc Insured Youtube

Robinhood Checking And Savings What We Know

Sipc Securities Investor Protection Corporation Sipc Insurance

Bill Winterberg Cfp On Twitter Robinhood Never Wrote That Their Checking Savings Feature Was Sipc Insured They Write That All Robinhood Brokerage Accounts Are Sipc Insured It S True The Problem Is

Sipc Securities Investor Protection Corporation Sipc Insurance

What Happens If M1 Finance Goes Out Of Business Investing Simple

Make The Most Of Your Free Fdic Insurance Investing Us News

Bank Failure Will Your Assets Be Protected

Robinhood Walks Back Checking And Savings Product

Fdic Vs Sipc Insurance 8 Things You Need To Know Today Chief Mom Officer

Sipc Securities Investor Protection Corporation Sipc Insurance

Horrific Housing Secret Elevator 2020

How To Animate In Roblox Sheasu

Baldis Basics Game Roblox

Roblox Ad Template 728x90

Baldis Basics Roblox Badges

125cc Hero Glamour Price In Kolkata

Aesthetic Roblox Boys Outfit Codes

Aesthetic Emo Roblox Character

Fortnite Item Shop Today June 12 2020

Wika Wiki Mansion

Roblox Magic Revelations Script

Roblox Jailbreak Gui Script 2018

Roblox Retail Tycoon Hack 2018

Redboy Download

Discord How To Add Bots To Your Server

Aesthetic Boy Roblox Outfit Codes

Roblox Bus Simulator Wiki

Who Was The Creator Of Roblox Name